No need to say it, it goes without saying, it should be obvious to all but, just in case it isn't obvious to all, IDA is dead.

IDA is the Cabinet Office Identity Assurance programme. And it's dead.

----------

"This week a small group of people became the first users to sign in to a government service using identity assurance". That's what Steve Wreyford of GDS said. The best part of five months ago. 11 February 2014, Identity assurance goes into

"This week a small group of people became the first users to sign in to a government service using identity assurance". That's what Steve Wreyford of GDS said. The best part of five months ago. 11 February 2014, Identity assurance goes into intensive care beta.

The beta test was a private affair. Close family only. GDS (the Government Digital Service), with just HMRC (Her Majesty's Revenue and Customs) and DVLA (the Driver & Vehicle Licensing Agency) in attendance.

GDS turned up at a

GDS turned up at a funeral for conference on the mooncalf economics of identity on 9 June 2014 where they tried to attract new investors, for all the world as though IDA was still alive. The book was dutifully talked up by GDS's brokers, OIX (the Open Identity Exchange) and KPMG. They even got Francis "JFDI" Maude to say:

And then on 30 June 2014 we were advised that there is at last a Private beta demonstration available to the public. It was Steve Wreyford again, linking us to OIX and to a video made at the mooncalf conference. A video of GDS's Janet Hughes talking us through IDA:

The video is worth watching. Several times. The presentation comprises 16 slides and there is a set of screen shots available.

The idea is that we shall all need one or more on-line IDs to use public services. Public services should become digital by default. No on-line ID, no services.

What Janet Hughes is presenting is the current thinking on how we mooncalves might go about obtaining on-line IDs (or "profiles", as GDS have taken to calling them).

What Janet Hughes is presenting is the current thinking on how we mooncalves might go about obtaining on-line IDs (or "profiles", as GDS have taken to calling them).

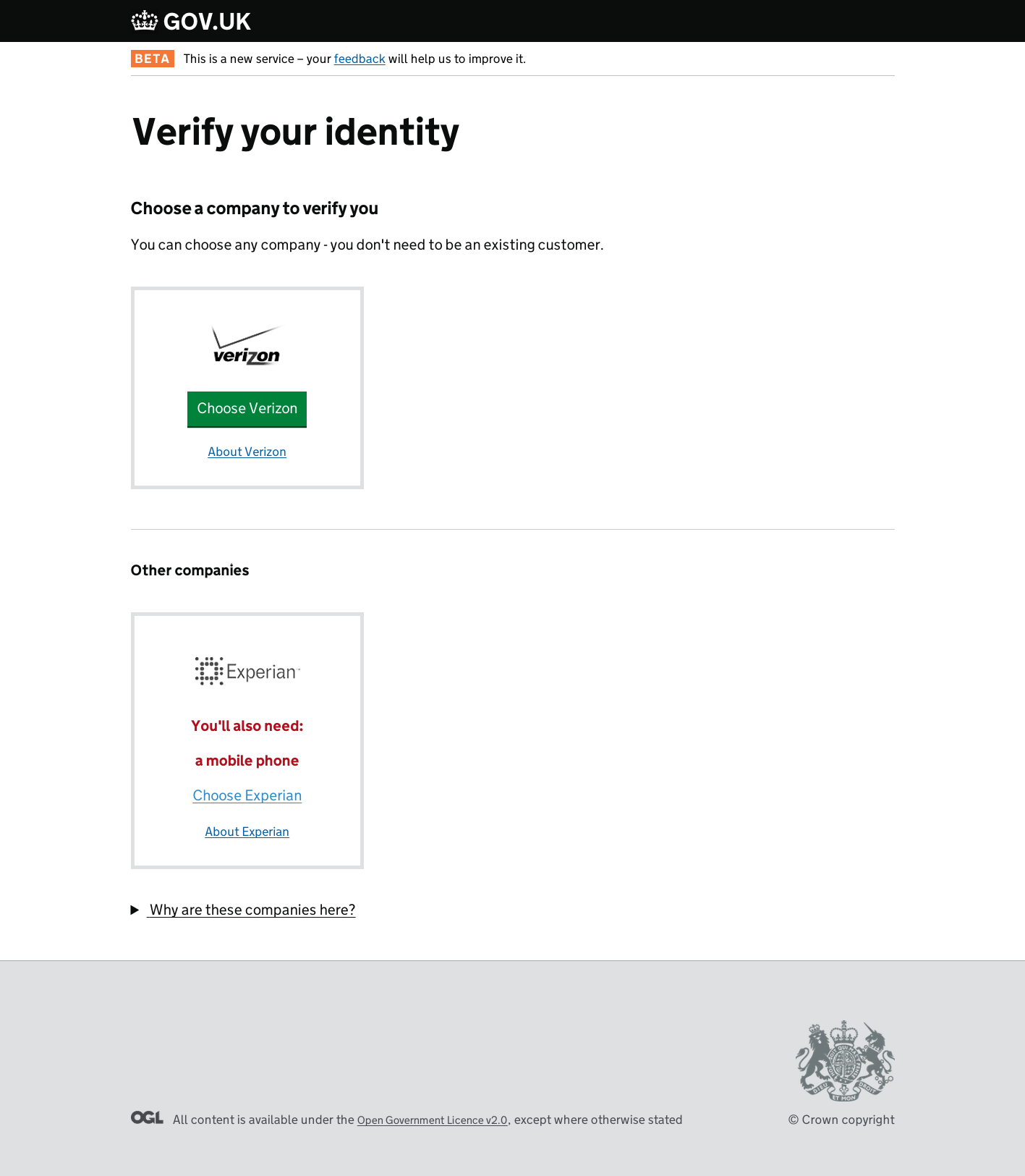

The idea is that our on-line IDs should be provided to us by so-called ... "identity providers".

We were led to believe until recently that there are five "identity providers". Judging by this presentation, there are only four left, please see slide #1, Mydex has disappeared.

GDS want to recruit more "identity providers". Thus the mooncalf conference. It's a brave candidate who will put his name forward now, in a field that started with 80 runners and riders/expressions of interest, which then shrank to eight, and from which competent experts like PayPal and Cassidian have subsequently withdrawn.

The application procedure for an on-line ID as demonstrated on 9 June 2014 raises a few hundred questions. Let's make a start with slide #5, which includes this:

To check your identity we need to securely connect to your bank, your credit record, your government records [and] your utility suppliers. This information is not stored by Post Office [one of the four remaining "identity providers"] – it is only used to confirm your identity. I give permission – continue.

To check your identity we need to securely connect to your bank, your credit record, your government records [and] your utility suppliers. This information is not stored by Post Office [one of the four remaining "identity providers"] – it is only used to confirm your identity. I give permission – continue.

By this stage in the application procedure, slide #5, you haven't told GDS who your bank is or who your utility suppliers are. You certainly haven't handed over any logon IDs or passwords to access your accounts.

And yet here's an "identity provider" warning you that they're about to connect to your bank, your utility suppliers, unspecified government departments and unspecified credit referencing agencies to check your details.

Does that mean what it says?

Have the banks and the utility companies and the credit referencing agencies and government departments granted access – access to your personal information – to four companies, the "identity providers", without asking your permission or even, until now, telling you?

"We're building trust by being open"?

----------

Updated 9.9.14

"GDS want to recruit more 'identity providers' ...", we said above, back in July, "it's a brave candidate who will put his name forward now ...". It's September now and this has just arrived, Procurement 2: timeframes and market briefing event, an invitation to a briefing for brave candidates to take place on 30 October 2014.

Book early to avoid disappointment. DMossEsq has. No more than two brave representatives per brave organisation.

NB

The identity assurance team have got their identity wrong.

They say to book by sending an email to idap_procurement_2@digital.cabinet-office.gov.uk. But if you click on the link, your email goes to idap_procurement_2@digital.cabient-office.gov.uk, an address which doesn't exist, an "invalid domain", as they say.

"We're building trust by being open".

(The NB above was added at about 10:00 a.m. The link has now, about 11:55 a.m., been corrected.)

Updated 8.10.14

From AccountancyLive.com, 17 September 2014, hat tip Toby Stevens:

Do you remember being consulted about Digidentity, Experian, Mydex, the Post Office, Verizon and other unnamed organisations collecting all your personal details and then selling them to the government?

"We're building trust by being open".

Updated 9.10.14 #1 of 2

How would IDA work if it existed?

IDA is the Government Digital Service's mythological identity assurance scheme, also known for the moment as GOV.UK Verify, which is meant to allow everyone to communicate with the government on-line, e.g. to apply for benefits. With IDA, the idea is that the government will know that you really are who you say you are.

How could they know that?

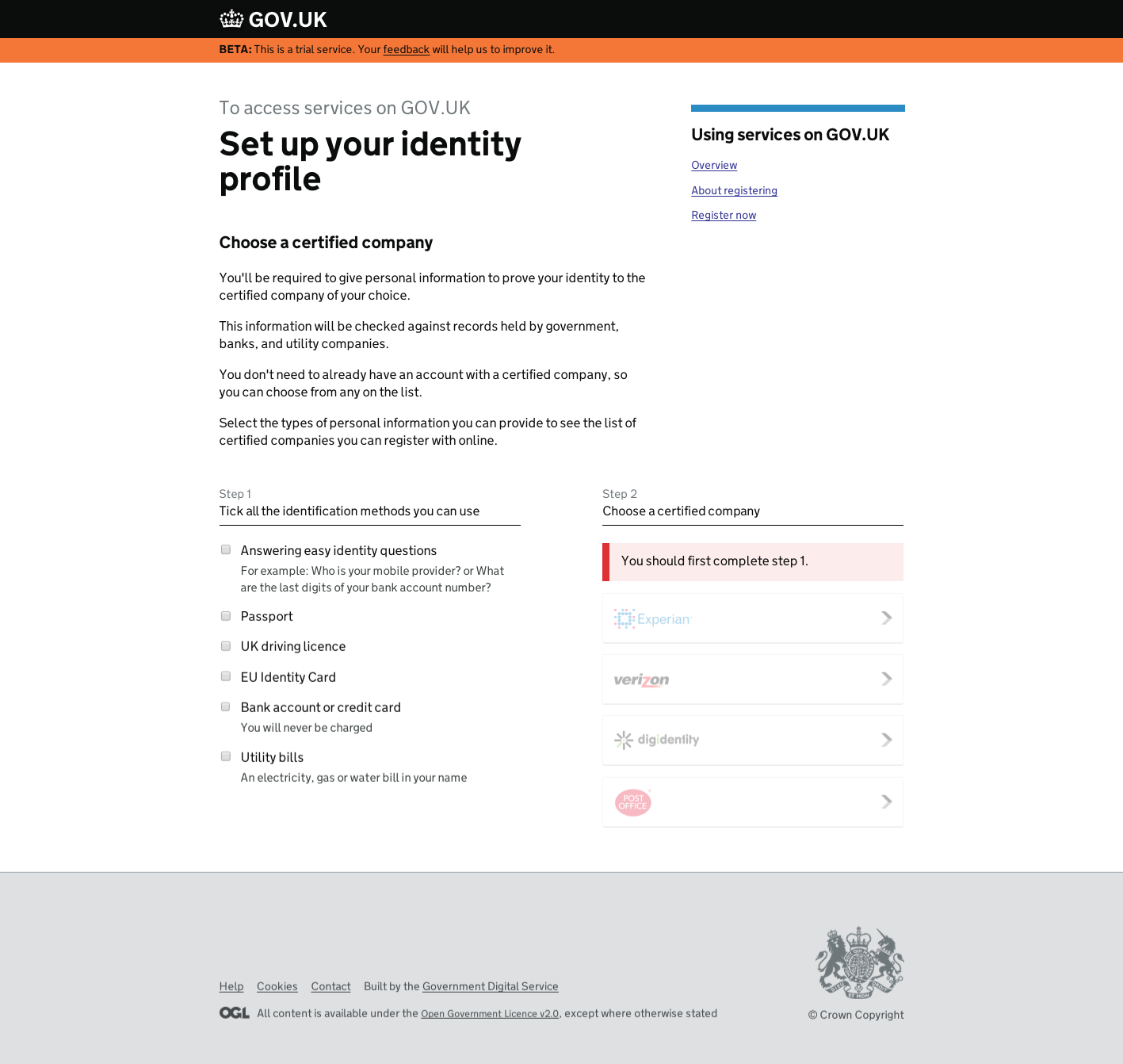

GDS blogged about this matter yesterday, How certified companies verify your identity, and also published a Guidance Note, GOV.UK Verify: checks identity providers must perform.

The companies referred to in the blog post are the spookily named "identity providers" that GDS is trying to saddle us with – Digidentity, Experian, Mydex, the Post Office and Verizon. Experian are certified by tScheme. None of the other IDPs are. So much for the blog post.

Moving on to the Guidance Note, GDS say that IDPs will need to confirm your name, address, date of birth and gender. They may also need your driving licence or bank account details. Do you want to give your bank account details to Digidentity? Do you have any idea who Digidentity is? Is that really Digidentity collecting your answers on-line or is it a website pretending to be Digidentity's?

There's no answer to those questions. And there are more. More questions. A lot more.

The IDPs need to "verify" your identity by checking your biometrics or by checking that you look like your photograph or by doing a knowledge-based test. That's what it says in the Guidance Note.

You can forget about biometrics for the next couple of decades. No-one has been collecting them in sufficient quantity and mass consumer biometrics don't work anyway. The physical verification against a photograph, for example, can't work on-line. So that leaves us with the knowledge-based tests.

What could they be?

There is no hint of an answer in the Guidance Note.

But as luck would have it DMossEsq has three times had to undergo such tests, twice when his bank account was defrauded and once when he lost his credit cards.

There were lots of simple questions, on the phone rather than on-line but it comes to the same, about his address and his age and whether such-and-such a bank account was in joint names or not.

And then, this: "I'm going to read out a list of names and I want you to tell me which if any of them has been a tenant at <address>". The person at the other end of the line knew that DMossEsq owns a house at that address, and knew that it was tenanted and knew the names of some of the ex-tenants going back years. How? What else did they know? DMossEsq's bank wouldn't be party to that information. Where were they getting it from?

That is the kind of knowledge-based verification which you may expect IDA/GOV.UK Verify to rely on.

Digidentity just can't have that sort of information about people who live in the UK – they're a Dutch company. Similarly, Verizon is American. Mydex is too small. The Post Office has no reason to have that sort of information about DMossEsq nor, possibly, about you either. So where is this information supposed to come from?

The only answer that DMossEsq can come up with is ... the credit referencing agencies, such as Experian. The other IDPs must go to the credit referencing agencies for this information. Otherwise IDA/GOV.UK Verify just can't work.

We know that the credit referencing companies – or "data brokers" as they call them in the US – collect data from a large number of sources to establish credit ratings for individuals and for organisations. They also help political parties to target selected types of voter. And they help marketing organisations generally to target their campaigns. That's their job.

They don't provide their services for free. Quite right, too. So Digidentity, Mydex, the Post Office and Verizon must pay for them. Either that, or GDS must pay on their behalf and, indeed, GDS say that they are the only people paying the IDPs. In effect, GDS are aiming to buy the use of remarkably "personal and pertinent" information about us all.

Despite GDS's claim that "we're building trust by being open", this may well be the first you've heard of knowledge-based verification. It would be a monumental change to the way we live. GDS have done nothing to prepare the public. And according to GDS, the first IDA/GOV.UK Verify services are due to go live this month.

You can forget that obviously. RIP IDA.

But you may still have some questions about GDS relying on the IDPs and the credit referencing agencies and Google and Facebook and Amazon and Apple and PayPal and the banks and the insurance companies and the utilities and the travel companies and the mobile phone companies collecting huge quantities of information about you and then trying to make money out of it.

Germany certainly has questions. They've banned Verizon from government contracts, please see German government terminates Verizon contract over NSA snooping fears.

And the US has questions about Experian, please see What Information Do Data Brokers Have on Consumers, and How Do They Use It? or, if you haven't got time to watch it all, try RIP IDA – 16 June 2014.

Do GDS have any answers?

Updated 9.10.14 #2 of 2

"Do GDS have any answers?", we were asking.

Some.

They've published a post on their blog, Information for companies interested in becoming identity providers. That has links in particular to:

What is now clear to the public for the first time is that IDA/UK.GOV Verify depends crucially on credit referencing agencies and other data aggregators/brokers. The public have not been prepared for that by GDS and the reaction may be shock.

The chairman or chief executive of any company interested in becoming an "identity provider", interested in protecting the brand that company has established over the years and interested in one day becoming the chairman or chief executive of another company is recommended to sit this one out – the shocked public includes shareholders and equity analysts and, in some cases, your mother.

Updated 10.10.14

GDS, the Government Digital Service, are famous for their ambivalent attitude to security. They don't really like it. It's inconvenient.

It came as no surprise, therefore, when they published the Identity Proofing and Verification Operations Manual despite the fact that it is clearly marked "Commercial In Confidence". As we said at the time:

They changed it.

GDS changed the document.

The first version DMossEsq saw is available here with "Commercial in Confidence" at the top of each page. And here's the later version, with that text removed.

Is the content confidential or isn't it?

Is the content commercial or isn't it?

Don't ask GDS. They just want it to be convenient. We know that. They've told us. Repeatedly. Just to reinforce the point, Tom Loosemore, the deputy head of GDS, derided the mythology of security in his recent speech to the Code for America conference (7'00"-8'25").

Any prospective "identity providers" will just have to learn to take the rough with the smooth, securitywise, in their dealings with GDS. Sometimes an agreement will start the day confidential and end it published on the web.

And anyone using IDA/GOV.UK Verify who finds that their confidential personal details have leaked out of one of the IDPs' databases will have the devil of a job getting their security complaints taken seriously by GDS. Why take a myth seriously?

Updated 17.10.14

Three days ago GDS's Identity Assurance team celebrated a milestone: "we've completed all the work we need to do to go into public beta".

Three days ago GDS's Identity Assurance team celebrated a milestone: "we've completed all the work we need to do to go into public beta".

Trust

They're looking to inspire trust in IDA.

They've only got one certificated "identity provider" – Experian, who need to explain how a fraudster acquired the personal details of several million Americans from them,

Four other "identity providers" – Digidentity, Mydex, the Post Office and Verizon – have yet to be approved by tScheme, the certification agency. "As we go into our public beta, we will have one identity provider that’s certified for wider public use. By the end of the year we’ll have 4", say GDS. How do they know that three more "identity providers" will be certified? That's up to tScheme, not GDS. And which one will fail?

Verizon, of course, have been banned from contracts with the German government following the revelations of Edward Snowden. If the Germans don't trust them, why should the British?

Just because tScheme say an organisation is trustworthy doesn't mean that they will be trusted.

Delivery

IDA starts with something of a mountain to climb trustwise. And deliverywise.

"GOV.UK Verify has been in private beta since February", they say, and "We’ve built GOV.UK Verify based on more than a year of user research, iteration and development". The timeline doesn't go back to February or even to a year ago, October 2013. GDS and the Cabinet Office have been promising for years that IDA will soon be ready. IDA was part of the G-Digital Programme once, According to their January 2010 report, G-Digital Market Investigation High Level Analysis & Findings, the Cabinet Office were actively seeking "identity providers" five years ago. So far, they've got just one and there's still no sign of IDA.

Users

So there are no IDA users. There are no IDA-enabled services to use. GDS tried testing IDA in Warwickshire. "Users often struggled as they sought to understand how this method of signing in to government services worked", says the Warwickshire report, and "some aspects of the registration processes proved annoying to the users".

Meanwhile, GDS have been letting services loose on the public with no identity assurance. You can apply to register to vote in the UK, on-line, with no on-line identity assurance. You can apply for a student loan and for a power of attorney ditto. Are GDS to be praised for releasing those services or criticised for doing so with no identity assurance?

Delivery is GDS's watchword – the strategy is delivery. By that token, tiger or no tiger, for the past five years or so there seems to have been something wrong with the strategy. No trust, one "identity provider", no services, no users and nothing delivered. RIP IDA.

Updated 18.10.14

Back in the old days, July 2002, the Home Office issued a consultation document, Entitlement Cards and Identity Fraud – A Consultation Paper. The suggestion was that, as far as the government is concerned, when it comes to public services, a person is a set of entitlements. You are your entitlements? It didn't really work, and as a result of the consultation the Home Office changed the name from "entitlement cards" to "ID cards".

Eight years later, the scheme collapsed. In the interim, the answer to the question "who are you really?" had become "you are a set of biometrics, particularly your fingerprints and your facial geometry". At the scale required for 60 million Brits, the mass consumer technology then available was so wildly flaky as to be utterly unreliable.

Any ID scheme must take a view on how you first register someone and on how you subsequently verify that that is the person you're dealing with again, now that they want to register to vote or take out a power of attorney or whatever. What is the view of IDA/GOV.UK Verify? How do GDS hope to identity us and subsequently verify our identity?

Take a look at the 16 September 2014 report, GOV.UK Verify – Service Assessment. That's the report issued on the assessment of IDA on the strength of which GDS were allowed to proceed to a public beta. IDA is meant to make it such that "people can safely access their data and perform transactions when using digital public services, and government services can be confident to a defined level of assurance that a user is who they say they are".

How is IDA supposed to achieve that? "The [IDA] service team said that the twoIDPs [identity providers, only one left a month later] currently available cover around 75% of the UK population in terms of the evidence users are required to provide (users need to have a UK credit history or a passport/driving licence to verify their identity through GOV.UK Verify)".

GDS's answer to the question "who are you?" is "you are your credit history". "What is a person?", you may ask. "A person is a credit history", according to GDS.

Is that true? Can you see any problems with this definition of a person?

Updated 21.10.14 #1

The original post above was written over three months ago and finished by asking whether the banks and others had ever asked your permission to share data with GDS's "identity providers":

But point #1, what on earth is Ms Cuthbertson's bank doing, giving Experian or whoever the details of her standing orders and direct debits? Who said they are allowed to do that?

Why isn't Ms Cuthbertson furious?

If the "identity provider" was someone you'd never even heard of like Mydex, would you be a bit miffed if they knew how much you paid each month for your mortgage?

Even more so if, like Ms Cuthbertson, they knew and you didn't know or at least you couldn't remember?

Where have GDS got the idea from that this sort of intrusion is acceptable?

IDA/GOV.UK Verify won't work without it. GDS's identity assurance depends on intrusion. That doesn't make it acceptable.

The question hasn't even been raised yet in public. Are GDS hoping that it won't be raised? That everyone will just roll over and accept it? Is there a law somewhere that we haven't noticed that legitimises GDS's model based on intrusion or surveillance or the sharing of personal information with strangers?

So much for "we're building trust by being open".

Updated 21.10.14 #2

GDS are offering us a service which is supposed to allow us to transact with government departments safely. These government departments are sometimes known as "relying parties" or RPs. They rely on what the "identity providers" or IDPs tell them.

Identity assurance or IDA or GOV.UK Verify is supposed to allow the IDPs to give us a secure on-line ID with which we can deal with the RPs.

What happens when it goes wrong?

Never mind how it could go wrong, you know that somehow someone will manage to get hold of someone else's on-line ID – perhaps yours – and make money out of it.

What happens then?

We have quite a robust system at the moment whereby, subject to audit, the banks accept that the fraud has been perpetrated against them and that they are liable to compensate you.

That's the baby in the bathwater that GDS seem to want to throw out.

Under GOV.UK Verify, we have been told that all transactions will go through GDS's ID hub, please see RIP IDA – Obama fails to consult Maude. David Rennie of GDS announced that the ID hub is all the work of GDS and that the hub will be possessed of a property known as "unobservability":

That's unobservability for you and it means that IDA/GOV.UK Verify is unauditable.

When something goes wrong, there will be no way to assess liability.

Will GDS compensate you?

Why would they?

Perhaps David Rennie would like to explain. After all, "we're building trust by being open".

Updated 21.10.14 #3

It's not just individuals who deal with government. So do companies and partnerships and trusts and other organisations. And if public services are all to become digital by default, then they all need on-line IDs so that government departments can be assured as to their identity.

Identity assurance for organisations and their agents, it now transpires, is not a job for GDS's IDA/GOV.UK Verify. It's beyond them.

That's what GDS tell us in a blog post published yesterday, Identity assurance for organisations and agents.

That post contains one of the world's great contributions to the art of understatement.

Suppose you work in the accounts department at Royal Dutch Shell and t's your job to submit that company's VAT returns. You must be authorised by Shell to do that job. And HMRC have to know that Shell have authorised you to do it.

Hands up who thinks that Shell would agree to appeal to GDS for that authorisation.

As GDS themselves say:

Which means that IDA/GOV.UK Verify can only be at best one among many identity assurance schemes. One that depends, it seems, on the information that the credit referencing agencies compile about us and depends on sharing that information with a bunch of strangers over an unauditable ID hub.

What are GDS contributing?

RIP IDA.

Updated 30.10.14

We noted above that GDS have published the Executive Summary of the draft contract between them and the "identity providers". 94 clauses spread over 12 pages, it constitutes a veritable cornucopia of interest. A feast.

Let's start with a snack – clauses 85 and 86:

Come to that, what business is Verizon in?

The answer is given in an article published three weeks ago on AdExchanger.com, hat tip @NoDPIsigma: "Verizon bills itself as a triple threat. It’s got mobile, it’s got television, it’s got broadband ... it’s up to 103.3 million wireless customers, 6.2 million Internet users and 5.3 million TV subscribers. It’s a wealth of potential data that Verizon can use to power its advertising business".

IDA/GOV.UK Verify could add 60 million Brits to Verizon's collection.

Colson Hillier is Vice President of Verizon's Precision Markets Insight group and he says: "Ultimately, we don’t see ourselves as a data provider; we see ourselves as an ad platform that helps brands and consumers connect".

They don't work alone: "Verizon has partnerships with marketing data providers like Experian Marketing Services and Oracle’s BlueKai to enable anonymous matches between the Precision ID identifier and third-party data".

Having identified people and classified them using their own information or third party information from Experian and others, Verizon sell access to these people to organisations targeting particular segments. That may be for commercial campaigns or political campaigns.

It happens in the US, as the Times were telling us the other day, in connection with the mid-term Congressional elections, please see US parties harvest web data to tailor adverts for voters: "Voters in America are being served up millions of tailored online adverts as the political machines gather more data than ever". It could happen in the UK.

Precise marketing is not sold to the people registered under the auspices of IDA/GOV.UK Verify and so it is not constrained by clause 85.

Verizon and Experian are not offering identity assurance to the companies and political parties with the big marketing budgets and so this business is not constrained by clause 86.

The advertisers and the political parties pay good money for well-classified targets for their campaigns – please see for example Martin Sorrell: if you don’t eat your children, someone else will. That could explain why Verizon and Experian are interested in IDA/GOV.UK Verify, which pays very little.

Now roll forward six years to Rt Hon Francis Maude MP's speech at yesterday's Payments Council cyber security seminar:

What do GDS know about operating payment systems?

Come back Crosby.

Updated 31.10.14

According to yesterday's Computer Weekly, Problems surface as first users attempt to use Gov.UK Verify:

If they can't use the combined efforts of GDS and Experian to create an on-line identity, then they don't exist. And if they don't exist, then they can't have any problems, either with IDA/GOV.UK Verify or with the CAP.

In which case, there aren't any problems, either with IDA/GOV.UK Verify or with the CAP.

It's like that Rory Cellan-Jones at the BBC. He doesn't exist either.

Digital by default – the humans cancel out of the equation.

Updated 3.11.14 #1

Here is a short extract from Mr Bracken's speech to the Code for America Summit 2013. That speech was delivered a year ago on 16 October 2013:

He's talking about IDA, the identity assurance service, currently known as GOV.UK Verify, and he says "We have about eight or nine companies already providing identity to us". That statement was false at the time and remains false today, a year later. GDS have one "identity provider" – Experian – and only one.

"The first services run out with our tax system this month [October 2013]", he says. Again, false. The planned pilot of PAYE Online didn't take place then and it still hasn't done.

We were in need of veracity assurance a year ago, the reliability of statements about IDA needed to be verified. We still are and it still does.

Updated 3.11.14 #2

IDA/GOV.UK Verify has been in private beta for some months, so we are told, and is now in public beta, ditto. It remains hard to find any reliable information about the system.

IDA is apparently operating at DEFRA (the Department for Environment Food & Rural Affairs), where it has something to do with payments to farmers. Emily Ball is the customer communications lead on CAP, the EU's Common Agricultural Policy, and her blog posts are the nearest thing we have to a handle on IDA.

On 17 October 2014 she published Introducing GOV.UK Verify, replacing Government Gateway for new CAP schemes. The two opening paragraphs read:

In the comments below her post, that clarity disappears. Three times, she says there will be an alternative:

She obviously realises that this is confusing and she published a new blog post on 30 October 2014, The CAP Information Service – continuous improvement, where she says:

Which suggests that there is no alternative and anyone who can't get themselves an on-line ID using IDA/GOV.UK Verify jolly well is excluded – people like:

Other government departments, please note the IDA/GOV.UK Verify treatment in store for you.

And perhaps GDS and Experian would like to explain at the same time how the system was let loose on an unsuspecting public with so many faults despite months and years of agile testing.

Meanwhile, any supplier considering joining Experian in the "identity provider" club, take note.

Updated 3.11.14 #3

Some of the early users of DEFRA's implementation of IDA/GOV.UK Verify have been spooked by the "identity provider", Experian, asking them about credit cards the farmers didn't even know that they had. If they don't know, how does Experian know? And how come Experian knows the day the farmers moved into their house several decades ago?

This is all to do with the "knowledge-based verification" we referred to above.

Collecting this sort of information is Experian's business. It is provided to them by the banks and other suppliers – among other things, Experian get the electoral rolls for every UK local authority.

Experian then sell the information back to the banks and other customers, in the form of credit ratings, market analysis and contact details for commercial and political campaigns.

That may come as a surprise to some people. Understandably enough. But it has been going on for decades, it is probably legal and you'll probably find that you signed an agreement at some point, in the small print of which you authorised it.

Suppose that GDS one day manage to get a second, certified "identity provider" to operate IDA/GOV.UK Verify. Digidentity, for example. It is highly unlikely that you in the UK have ever signed any agreement with your bank or with Experian authorising them to disclose information to Digidentity in the Netherlands.

So what on earth is Emily Ball of DEFRA talking about when she says, in The CAP Information Service – continuous improvement:

The answer, in GDS's mind, is you.

Go back to the presentation of the Post Office's registration dialogue above. The bit where it says "To check your identity we need to securely connect to your bank, your credit record, your government records your utility suppliers. This information is not stored by Post Office – it is only used to confirm your identity. I give permission – continue".

That is GDS's and/or the Post Office's idea of you giving your informed consent.

Either you give your consent. Or you go without your CAP payments. It's not informed consent. And it's not free consent.

Also, Emily Ball says "the security questions asked by certified companies are all based on information they already hold about you" and the Post Office say "this information is not stored by Post Office". Which is it?

Welcome to GDS's new digital-by-default world.

Updated 3.11.14 #4

Apparently:

Updated 3.11.14 #5

"The GOV.UK Verify service allows users to prove their identity when accessing digital services". That's what it says in the GOV.UK Verify – Service Assessment. It's the opening sentence. And it's false.

The service was reviewed on 16 September 2014 and "after consideration the assessment panel have concluded GOV.UK Verify ... has shown sufficient progress and evidence of meeting the Digital by Default Service Standard criteria and should proceed to launch in Beta". There are 26 of those criteria. And GOV.UK Verify passed the lot.

Updated 9 November 2014 #1

The Times newspaper's lead story on 4 November 2014 was Virtual IDs for everyone.

Traditionally, GDS leads with the Guardian, but it took that newspaper until 6 November 2014 to come out with Charles Arthur's Gov.uk quietly disrupts the problem of online identity login.

They hit the ground running. The opening paragraph reads:

GOV.UK Verify is not available for use when you apply on-line for either a provisional licence or a replacement licence. Take a look for yourself at Apply for your first provisional driving licence and Replace a lost, stolen, damaged or destroyed driving licence and Renew your driving licence.

All three take you to Directgov pages (which aren't supposed to exist any more, but there they are) and none of them offers the facilities of GOV.UK Verify.

There is no sign of GOV.UK Verify there and the same goes for passport applications and tax returns.

Mr Arthur is simply wrong with his opening paragraph and the article never recovers. It was trivially easy to verify the accuracy of GDS's briefing and, like the Times two days before, he didn't bother.

Updated 9.11.14 #2

Mr Arthur has responded to the point made above. What does he say about failing to check GDS's briefing and misleading his readers as a result? Answer – nothing. He avoids the issue:

DMossEsq doesn't understand how GOV.UK Verify works? Undoubtedly true. GDS have told us very little about it. Some of what they have told us is false. Some of it is self-contradictory.

Has Mr Arthur helped his readers to understand how GOV.UK Verify works? You must be the judge of that. Suppose you had 30 seconds on BBC Radio 4's World At One to explain GOV.UK Verify. On the basis of his article, what would you say?

Does Mr Arthur understand how GOV.UK Verify works?

"Banks now following gov.uk’s lead", he says in his Guardian article. Nonsense. Wrong way round.

The banks have been using the credit referencing agencies to verify identity for years. The banks have been sending us one-time passwords on our phones for years, whenever we try to set up a new payee on our on-line current accounts, for example.

GOV.UK Verify is copying the banks. A point which Mr Arthur has misunderstood.

Is Mr Arthur so happy with the credit referencing agencies storing our personal data and selling it to GOV.UK Verify's "identity providers" to verify our identity that he doesn't think it worth highlighting this business? What does he have to say about GDS's knowledge-based verification (KBI)? Nothing.

GOV.UK Verify only works even in theory if the credit referencing agencies are allowed to keep us under surveillance by storing details of all our transactions. That's where the quasi-secret information comes from on the basis of which GOV.UK Verify is supposed to be capable of giving low-grade identity assurance to DEFRA and HMRC and DWP and other "relying parties" (RPs). Mr Arthur considers this to be of no interest to his readers.

We already have a way for people and companies to undertake authorised transactions with government – the Government Gateway.

Mr Arthur doesn't mention that. Instead, in the tweet above, he says that GOV.UK Verify is "like OAuth for identity".

If it's exactly like OAuth, then we don't need GOV.UK Verify. Why haven't GDS used OAuth? Why have they wasted their time and our money developing GOV.UK Verify?

GOV.UK Verify is "a world first" according to Mr Arthur's article. Here's a list of 59 users of OAuth. If anything, GOV.UK Verify must be "a world sixtieth".

If after all GOV.UK Verify isn't exactly exactly like OAuth, then in what way is it different? Or better? Mr Arthur doesn't tell us. Does he know? Or was the answer omitted from the GDS briefing pack which he so cravenly reproduced?

GOV.UK Verify "could have as many as half a million users with a year". Mr Arthur probably means "within a year". He mentions that possibility. He doesn't mention the problems Rory Cellan-Jones had, trying to obtain an on-line ID through GOV.UK Verify. Mr Cellan-Jones is the BBC's esteemed technology editor and he couldn't make GOV.UK Verify work.

And if he couldn't, what chance the farmers being forced by DEFRA to use GOV.UK Verify?

We know the answer to that. But Mr Arthur doesn't mention these problems. As far as his readers know there are no problems:

Updated 11.11.14

The putative attractions of GDS's GOV.UK Verify identity assurance scheme include the independent assessment of the "identity providers" by tScheme.

Take away tScheme's independence, and GOV.UK Verify looks even less viable, RIP.

Back on 17 October 2014 we had a question:

So much for independence.

Updated 13.11.14

"I work as a user researcher for GOV.UK Verify", says a person writing today on GDS's Identity Assurance blog, Using evidence from user research to redesign GOV.UK Verify.

"I work as a user researcher for GOV.UK Verify", says a person writing today on GDS's Identity Assurance blog, Using evidence from user research to redesign GOV.UK Verify.

The idea behind GOV.UK Verify is that it would be up to us users to choose our "identity providers". At least, that was the idea, but apparently research evidence now suggests that we really want to be told which "identity provider" to choose. That's what the blog says.

The reaction of the "identity providers" is not recorded. More research needed, no doubt, although we can surely guess in advance that if they're supposed to be operating in a free market they're not going to take too kindly to having their competitors recommended.

The "user researcher" for GOV.UK Verify says that there will be a couple of simple questions asked of us users and then "based on someone’s answers to these questions, we recommend a certified company that is likely to work for them". The example given in the blog recommends "Choose Verizon" – an odd choice, as Verizon hasn't been certified yet.

In fact, the lower quality, second recommendation – Experian – is the only answer possible as they are the only certified "identity provider".

Notwithstanding which, the blog says "we have contracts with 5 certified companies in total".

Which five "identity providers" does the blog have in mind? They're listed – Digidentity, Experian, the Post Office and Verizon. But that's only four.

Yet more research needed, but it's beginning to look as though Mystic GDS's prediction that one of the five companies will fail to be certified by the entirely independent tScheme is correct and points to the excommunication of Mydex.

Updated 14.11.14

GDS have a problem with security. They can't take it seriously.

GDS have a problem with security. They can't take it seriously.

Ditto privacy. All data should be shared. It's for our own good. Apps can make recommendations for the quantified self better than humans can decide for themselves. That's the Estonian thinking round at GDS Towers.

GOV.UK Verify is supposed to be subject to identity assurance privacy principles. Nine of them.

How well does GOV.UK Verify score? 0. 0 out of 9. And lucky to get that many.

Updated 18.11.14

No man is an island.

And no country either, as GDS reminded us the other day in Identity assurance in the European Union:

Now try this:

The regulation doesn't mean "that it will become possible for people in the UK to use GOV.UK Verify for online public services in other countries". Other countries will only let us Brits loose on their public services if they first believe that GOV.UK Verify works. And so far there is no reason for us to believe that. So why should the Bulgarian equivalent of Companies House, for example, believe it?

GOV.UK Verify currently offers low-grade assurance that you are who you say you are. Will Bulgaria accept that? Why would they?

Conversely, GDS are going to have to work out whether they accept the identity assurance of 27 other countries. How are they going to do that? And when?

Incidentally ...

... we've been here before. Project STORK:

Updated 2.12.14

Farmers who have trouble registering for their CAP payments are going to be angry with DEFRA.

In a way, that's unfair.

Registration requires the farmers to use GOV.UK Verify, Whitehall's identity assurance scheme.

Identity assurance is not a big enough project for the Major Projects Authority to worry about. Apparently. Even though it could affect every person and every organisation in the country.

But it is big enough to warrant its own blog, https://identityassurance.blog.gov.uk/:

It is GDS – the Government Digital Service – who are "responsible for GOV.UK Verify and other related products and services" and not DEFRA.

It is GDS – the Government Digital Service – who are "responsible for GOV.UK Verify and other related products and services" and not DEFRA.

The fair criticism is that DEFRA let GDS threaten DEFRA's own parishioners. They shouldn't have done.

DEFRA is the Department of the Environment Food and Rural Affairs and they're meant to look after farmers. Not expose them to impossible computer systems with no alternative method of registration provided.

Updated 3.12.14 #1

How does a certified company establish that it’s really you?, they were asking 10 days ago, over on the GOV.UK Verify blog.

GOV.UK Verify will give access to your passport and driving licence records, we are told, to a bunch ofidentity providers certified companies, many of whom you've never heard of, many of whom are already under contract even though they haven't been certified.

These certified companies will check your credit reference. Remember, in GOV.UK Verify, you are your credit history. A person is a credit record.

It's not clear how the economics work. Experian is an "identity provider". It is also a credit reference agency. It can access your credit history for free if that's how it cares to account for its GOV.UK Verify business. But suppose Mydex want to access your credit record. Do they have to pay Experian? Or Equifax? There's not much money in the GOV.UK Verify pot. And there's no reason for Experian or Equifax to give Mydex free access. How is this tension going to be relieved?

The certified companies will also make use of quasi-secret information about you:

That's certainly the view of Mydex. They are the champions of giving people control over their own data. So they say. Although they can never explain how they can give you control over your own data.

How are they going to stop Verizon from selling your data? Remember Verizon's words: "Ultimately, we don’t see ourselves as a data provider; we see ourselves as an ad platform that helps brands and consumers connect". What sanction do Mydex have over Verizon? None.

Mydex and Verizon are both "identity providers". But not certified companies. tScheme haven't finished evaluating them yet.

But there was big news yesterday – GOV.UK Verify has a second certified company. Digidentity.

Who?

You may well ask.

They're a Dutch company. So they're unlikely to have much data about 60 million of us Brits. So where are they going to get the data to verify our identities? And how are they going to pay for it out of GDS's modest budget?

Remember, in this strange market in identity assurance, which people keep referring to as an "ecosystem", GDS are the only people allowed to pay.

You've never heard of Digidentity and Digidentity have never heard of you. But somehow they're supposed to assure HMRC or whoever that you're you.

Lots of questions. No answers. And yet GDS expect people to make an informed choice between Experian and Digidentity when it comes to choosing their "identity provider". How? Why do GDS expect that?

Don't think the questions stop there.

Two days ago, GDS published How we’re working to increase the range of data sources available for GOV.UK Verify:

Remember midata? The Department for Business Innovation and Skills initiative that was going to "kickstart an inflection point in business"? They wanted to use your education, travel and health records. You mustn't mind. It's all for your own good. And to help the economy to grow.

If you've forgotten, and you don't mind being spoken to like a cretin, watch this – you lose control of your education, travel and health records about two minutes into this 2'57" video for mooncalves:

But surely, you may say, midata is all over, finished, washed up. It's more than a year now since we last heard from Craig Belsham and his midata Innovation Lab, 28 November 2013.

But that's not how it works. Do try to keep up. Now we have midata studios, please see the recently released MiData Studio Feasibility Summary Report November 2014. Lab? Studio? Who cares? Just so long as we all freely give our informed consent to have our passport, driving licence, education, travel and health records shared with everyone.

David Gauke MP thinks it's a good idea. So does Rt Hon Francis Maude MP. And presumably Vince Cable, President of the Board of Trade. Not to mention the Information Commissioner. And Stephan Shakespeare and Tim 'long live the database state' Kelsey. And Nigel Shadbolt, the chairman of the midata programme and chairman of the Open Data Institute. They all think that open data is magic.

If you disagree, that means you want children to be unhappy and you want people to die of cancer. That's what Stephan Shakespeare says. So you will let certified companies establish that you're really you, won't you.

Updated 3.12.14 #2

You may be reluctant to share all your personal information with GDS's "identity providers". Even if they are now known as "certified companies".

You shouldn't be so insular.

Through the good offices of Project STORK, your information will actually be shared with every country in the EU:

Updated 4.12.14

Remember two days ago? When Digidentity joins GOV.UK Verify public beta as it says on GDS's identity assurance blog?

And who certifies "identity providers"? tScheme.

And if we check the tScheme website, do Digidentity appear on the directory of approved services? No. So they'e not a certified company.

So how did GDS reach this "milestone" of theirs? GDS, who, remember, are "building trust by being open"?

And what do Digidentity have to say on their website about GDS, tScheme and GOV.UK Verify? Nothing. Not a single mention. Google it.

Updated 12.12.14

There we were on 4 December 2014 pointing out that what the Government Digital Service said was wrong.

They said:

Digidentity are not a certified company.

Companies are certified when tScheme say so and Digidentity do not appear on tScheme's directory of approved services. Digidentity remain on tScheme's directory of registered applicants, where they have been since 24 February 2014.

Not sure about the importance of tScheme?

GDS published What it means to be a ‘certified company’ yesterday:

GDS have undermined tScheme, whose independence must be unquestioned if their certificates are to inspire trust.

GDS have undermined Digidentity, who must be seen to speak for themselves. Instead, here's GDS speaking for them.

GDS have undermined themselves. "We're building trust by being open"? That's not what it looks like.

GDS are trying to attract new certified companies (previously, "identity providers") to join their identity assurance initiative, GOV.UK Verify, please see Making sure we have a range of certified companies. The reputational risks any new recruits would be taking are mounting by the day.

GDS hosted the first meeting of the D5 this week. The UK, Estonia, Israel, South Korea and New Zealand all joined together to "celebrate" digital government, including GDS's two-years-late-and-still-not-working GOV.UK Verify public service. They've all just signed a charter of principles. What kind of a principle is demonstrated by pretending that you've got two "identity providers" when in fact you've only got one, Experian?

Come to that, what was GDS's executive director talking about a year ago when he told a conference that GDS had eight or nine "identity providers"?

GDS have been asked to comment on the Digidentity question:

It's not up to GDS to say that Digidentity are "fully compliant". It's up to tScheme.

"Formal certification due shortly", say GDS. So it hasn't been granted yet. They were wrong to say 10 days ago that it had already been granted.

If this is the "normal process" for GOV.UK Verify, as far as the public is concerned, RIP.

Updated 18.12.14

GDS only have one certified "identity provider" for their GOV.UK Verify identity assurance service (RIP). They need more. Yesterday, they announced details of their invitation to tender, Procurement update. There is a summary on the Guardian newspaper's Government Computing website, GDS launches second GOV.UK Verify framework.

GDS are offering up to £150 million for up to 10 "identity providers" to verify the identities of up to 60 million Brits for up to four years. Suppose everyone registers with all 10 suppliers. That's 600 million registrations. 25 pence each. 6 pence-and-a-farthing p.a. For that, GDS expect to buy Level of Assurance 2 (civil courts) and may ask for Level of Assurance 3 (criminal courts).

There may not be that many registrations, of course. On the other hand, the number of verifications that have to be performed afterverification registration could be huge. Suppose we all use our "identity providers" to transact with the government 10 times a year on average. That's 600 million verifications p.a., 2.4 billion verifications over the four-year period – 2.4 billion times the "identity providers" put their head on the block and assure the government that you are who you say you are.

600 million registrations. 2.4 billion verifications. Any supplier responding to this invitation and submitting a tender must explain to their shareholders how they and their sub-contractors can take on the onerous liabilities of the identity assurance contract and make a profit out of 6¼ pence. Those explanations should make interesting reading.

It's not just the investors in private sector "identity providers" who will need to be convinced of the reality of this dream. If GDS are to be believed, 27 other EU governments are going to have to buy into the fantasy, please see STORK: a practical way to access services across borders. Do you see Germany, for example, relying on 6¼ pence-worth of identity assurance?

Updated 22.12.14

For two weeks or so now, we have all watched as Sony's private and confidential correspondence has been published by hackers, personal details about the stars of their films have been revealed and the value of the company's intellectual property has been destroyed.

It's not the first time it's happened to Sony and Sony aren't the first organisation it's happened to – we are fed a daily diet of on-line security breaches with stories coming from all over the world. Banks, retailers, government departments, ..., they all, like Sony, make their best efforts to preserve on-line security and they all fail. Even defence contractors get hacked. And they're meant to be the experts.

Salesmen keep on trying to ply their on-line wares on the basis of secure websites. Sometimes they go further and offer supersecurity. Even hypersecurity. But it must finally dawn on them, as it has on everyone else, including Sony, that there just is no such thing as a secure website. Unicorns don't exist. And neither do secure websites.

On 9 November 2014, GDS offered us all GOV.UK Verify, "a new 'verified identity' scheme ... allowing users to register securely using one log in that connects and securely stores their personal data". Who is ever going to believe that tired old marketing line again? Remember Sony. No-one.

Here's a prediction. By the turn of the year, it will look suspicious to offer secure websites. Any sales organisation relying on that offer will be a laughing stock. 2014 will prove to be the last year any respectable organisation tries to maintain the pretence.

Updated 28.12.14

Father Christmas may or may not exist but secure websites certainly don't.

Sony PlayStation struggling to restore network after Christmas hacking attack, the Telegraph newspaper told us yesterday, and followed it up with Hackers 'leak details of 13k users of PlayStation, Xbox and Amazon':

In a reversal of the classical model, only the adults believe in web security – the children know it doesn't exist. The so-called "modernisation" of government, making all public services digital by default, is more properly termed "infantilisation".

Updated 19.1.15

As every fule kno, "UKGovcamp is the free, annual 'unconference' for people interested in how the public sector does digital stuff". The hashtag for this year's unconference is #ukgc15, obviously, and the following plaintive call has been issued:

Campers may care to inform themselves in advance of the festivities by taking a peek at GDS: We might miss our digi-goal. Quick, MAKE IT BIGGER in today's ElReg:

Updated 20.1.15

There's a lot to think about in Neil Merrett's latest Kable/Government Computing article:

The Government Digital Service now claim that all five "identity providers" will be accredited by April 2015. Whereas, on 14 October 2014, GDS told us that:

Remember, you can keep score yourself via the tScheme website. "Identity providers"/certified companies are only certified if tScheme say so. It's up tScheme to certify their trustworthiness, not GDS. tScheme are meant to be independent and GDS impugn that independence every time they predict the numbers and the timing of certification. Right now, tScheme show just one approved service for IDA – Experian's. The other four "identity providers" – Digidentity, Mydex, the Post Office and Verizon – are still firmly on tScheme's registered applicants list and thus not accredited or certified or ... trustworthy.

Next on Mr Merrett's list, note that the five "identity providers" left in the running, down from eight originally, are contracted under the current IDA framework. Soon there will be a new IDA framework. And then the "identity providers" will have to apply all over again for accreditation. And they may face competition from any number of other prospective suppliers.

Why bother to apply again? Why would anyone else bother to apply? Why did Cassidian, Ingeus and PayPal pull out? What will the equity analysts make of any company applying under the new IDA framework? What will their shareholders make of it? There's very little money on offer – £150 million to register everyone in the country and every organisation. Where's the profit supposed to come from? What are the risks? What about all the other competing identity schemes? Why haven't GDS provided identity assurance for electoral registration? (Show, don't tell, how's that going?) Why has the identity assurance GDS provided to DEFRA been abandoned? Can you do identity assurance business with an organisation – GDS – that is simply uninterested in security? To repeat, why bother?

Mr Merrett has an elliptical way of writing. His clear and sparse prose includes all the questions above and more.

Finally, Mr Merrett tells his readers that GDS intend to find more ways to register us all and make it easier to identify us on-line. Sticking to the credit rating data held by Experian gives GOV.UK Verify a 60% success rate or, to put it another way, a 40% failure rate. Perhaps if we give GOV.UK Verify access to our bank accounts as well, and our mobile phone records, that might improve the successful registration rate.

It might.

In which case, why not open up completely? Why not throw confidentiality and privacy to the winds? And caution and dignity and maturity. We could add our health records. And our educational records. And our travel records. As noted above. That ought to make life easier for GDS. And for the hackers.

And that's dealt with just Mr Merrett's opening paragraphs.

Read him early. Early and often.

Updated 1.2.15

Read Mr Merrett early, we suggested immediately above, and read him often. As if to help with reading him often, Kable/Government Computing re-published his 20 January 2015 article nine days later under the title GOV.UK Verify constrained by need for more datasets.

GOV.UK Verify will work – that's the suggestion – if and only if you open up more and more of your life to GDS's so-called "identity providers". We know that that's false. You could reveal everything about yourself and yet Whitehall and local government could still fail to provide adequate public services.

Just ask the victims of the Child Support Agency, for example. The CSA had access to financial, medical, educational, social services and police records and yet they still managed to inflict misery on millions and failed to get children supported.

You would keep your part of the bargain only to find GDS renege on theirs.

Mr Merrett repeats, with an admirably straight face:

When you check, you'll see that tScheme have added a new member to their club of approved services – Equifax, another credit referencing agency, like Experian.

Equifax are not on GDS's list of "identity providers" to GOV.UK Verify. What does that tell you?

It tells you that GOV.UK Verify is just one identity assurance scheme among others, GDS face competition, other organisations like BT and RBS and the Metropolitan Police and the Home Office have been doing the job better and for longer than GDS. Why would a prospective new entrant to the identity assurance market sign up to GOV.UK Verify's list of "identity providers"? They don't need to. It would impose an unnecessary constraint on their perfectly viable, independent service.

It also tells you that when you look at the class of "identity providers", you're looking at organisations like the police and the Home Office. You may not have thought of the credit referencing agencies like that before, as an arm of the state, but there you are, there's the evidence.

What was that we were saying back on 18 October 2014? Oh yes:

GDS do have another credit referencing agency on their dwindling list of five "identity providers". Not Equifax, but Verizon. Nonsense. Editorial failure. Verizon is not a credit referencing agency. N And how do Verizon see themselves? Not as an arm of the state. Oh no:

Confusing, isn't it. Read Mr Merrett. Read him early. And read him often.

Updated 13.2.15

This time it's Submissions for new GOV.UK Verify framework to close on Monday. Neil Merrett. Read him early. And read him often.

Will any organisations be reckless enough to submit applications to become "identity providers" in GDS's new GOV.UK Verify framework? If they do, sell them short. (NB DMossEsq is not licensed to give investment advice.)

Mr Merrett repeats some of his favourite material, e.g. "At present, only Experian and Digidentity are accredited to provide ID assurance as part of the service's public beta". Experian's service has been approved by tScheme. Digidentity's still hasn't, it is still a mere registered applicant. In what sense is the "identity provider" Digidentity "accredited to provide ID assurance"? None. That accreditation is a figment of GDS's imagination (a figment repeated on their brand new service dashboard on the performance platform).

Mr Merrett again warns his readers that GDS want GOV.UK Verify to be able to process more of your personal information than just credit history, passport and driving licence: "Janet Hughes, programme head for GOV.UK Verify has previously explained that a key focus of the second assurance framework was to extend the number of datasets currently available to prove a user's identity through the platform".

Would it be wise to open yourself up in this way? What benefit do you get by letting GOV.UK Verify have access to your banking records, and mobile phone and energy usage and health and education and travel records? Would that improve public services? In what way? Would it transform government? Into what?

There are obvious dangers in allowing access to all this information about you through one framework.

You could become entirely dependent on GOV.UK Verify to do anything. That is the objective of Mydex, for example, one of GDS's "identity providers" – no Mydex, no transactions. Mr Merrett does warn you: "Mydex, which today said it expects to gain required accreditation to support Verify in the 'near future', also confirmed it would be submitting documentation to tender for the second iteration of the ID provider agreement before Monday's deadline".

You could open yourself up to fraud. All those personal details which identify you on-line equally allow fraudsters to pretend to be you on-line. There seems to be no defence against cybercrime. Remember Sony. Anyone offering you security on the web is locked in the last millennium.

And here we see Mr Merrett at his very best: "Sources involved in the accreditation process for GOV.UK Verify have previously suggested that GDS had perhaps been too rigorous in setting security standards required for ID providers wishing to support the first framework".

Never has humour been drier.

Which "sources" are these? No-one has ever accused GOV.UK Verify of being too secure. No-one ... with the possible exception of GDS themselves, who can't take security seriously and who seek to elevate usability above all.

Security breaches are guaranteed. People are going to suffer. Even security experts are helpless. What chance do you stand? In that case, when it happens, which it does every day, what happens?

If your bank account is emptied by fraudsters and it's not your fault it's deemed in the UK to be a fraud against the bank. Not against you. They suffer. But they have to compensate you. And they do. Again, it happens every day. That is the liability model we have got used to in the UK.

Do you think the same applies to GOV.UK Verify? If so, why do you think that? You've made an assumption. And you're wrong. Mydex gave evidence to the House of Commons Science and Technology Committee on 5 June 2013 during which they asserted that since their users hold the private key to their own personal data store, if there is a fraud perpetrated, it is unlikely to be Mydex's fault. No liability on Mydex's part, the fault lies with you (para.5).

This issue of liability has been taken up by the law firm Pinsent Masons: " ... financial services litigation and compliance expert Michael Ruck of Pinsent Masons ... said that although regulated firms [e.g. banks] can rely on third parties' due diligence, the approach carries risk as 'responsibility and any liability for failures remain' with those regulated businesses ... 'The bank, or any other regulated firm, can rely on third party checks but this does not escape any liability on the bank’s behalf,' Ruck said. 'Therefore any such reliance would require the bank to check, observe and review the activities of any such third party and be sure that it was conducting the appropriate due diligence' ...".

GDS's approach is insouciant not only about security but also the law and market practice. Out of that insouciance GDS hope to build trust. Can that work? RIP.

Read Neil Merrett. Read him early. And read him often.

Updated 22.2.15

Suppose that you sign up to the Government Digital Service's identity assurance scheme, GOV.UK Verify (RIP), and that as the result of a security breach at your chosen "identity provider" you lose money – e.g. your state benefits are paid to someone else. Two questions:

Suppose you choose Digidentity. Take a look at their terms and conditions of business.

Question 1, who do you claim compensation from? Not Digidentity:

Slim.

It's not just that when you registered with GOV.UK Verify you clicked the button to confirm that you had read and understood the terms and conditions of business.

In addition, your case would rely on a breach of the contract between you and Digidentity. And there isn't one. Because you haven't paid for the service. As far as you're concerned, it's free. "You can't have a contract without consideration" – any stockbroker will tell you that, for free.

By all means, go ahead and sign up with Digidentity. But on your own head be it.

Perhaps there's no need to worry, though. If you click on the About Digidentity link in the screen above, you read:

Infallible? That's beyond the US State Department. And everyone else. But not, apparently, Digidentity. Believe that if you will.

This situation is often called "putting you in control of your own data" or "empowering you". You may believe that as well.

Update 23.2.15

Any brave soul who, despite the risks, tries to register with the Government Digital Service's identity assurance scheme, GOV.UK Verify (RIP), is presented with this:

15 minutes?

You're going to have to be a spectacularly fast reader.

In 15 minutes, you're going to have to get to grips with the Digidentity terms and conditions of business, 2,347 words, some of them Dutch.

That and the Experian documentation. Experian is a proper FTSE-100 company. Not for them the relatively casual Digidentity offering. Experian have terms and conditions (2,986 words, which they advise you to print and keep), they have a privacy policy (2,249 words) and some FAQs (1,008 words) and a Public Service Description of their Identity as a Service product (1,733 words).

You may enjoy question 11 in the FAQs:

You may also enjoy this extract from the Experian privacy policy:

And there's this in the terms and conditions:

And this:

But look, the minutes are ticking by, you haven't got time to cavil. Let's say you choose Experian rather than Digidentity and you click on About Experian. This is what you see:

"Experian holds secure personal and financial information on over 45 million individuals in the UK". Feeling secure? "The UK Government chose Experian as one of the first companies to help you access their services online". More secure still? "... you can trust Experian to hold your information", except that you can't. Experian unwittingly supplied a criminal with personal information for nine months. They only stopped when the US Secret Service brought it to their attention, please see Experian Lapse Allowed ID Theft Service Access to 200 Million Consumer Records.

DMossEsq warned you about this nearly a year ago. Data goes missing, even in the best of companies. These things happen. You know that. You've got about a minute left. Do you want to make sure that they go on happening? Do you want to increase the risk that they will happen to you?

Why? 57 seconds, 56, 55, ... What is the benefit to you?

Updated 24.2.15

Because we don't care about his future, because he doesn't have one, we sacrificed the shortest, fattest, ugliest, oldest and smelliest member of the DMossEsq editorial team yesterday and, purely in the interests of science, we made him register with GOV.UK Verify, choosing Digidentity as his "identity provider".

He has now given his name, address, date of birth, telephone number, passport number, driving licence details, email address, and so on to a completely unknown company claiming to be based in Holland.

Digidentity asked him for his bank account number and, incredibly, he gave it to them. Digidentity seemed to know that it was the correct number. How?

They also knew that he had taken out a mortgage in December 2001 and asked him to confirm the outstanding balance, which he did. How did they know that he had taken out this mortgage? How did they know what the outstanding balance is?

How did they know that he had taken out a Vodafone contract just over a year ago?

There is no way that Digidentity had this information at their fingertips. They must have got it from another organisation. Possibly Experian or one of the other credit referencing agencies. Our ex-colleague's personal information has clearly been flying all over the web.

Why bother to have Digidentity in the middle if the registration work is really being performed by the credit referencing agencies?

How much did Experian or whoever charge Digidentity for this information? How can Digidentity afford to pay for it and still have any profit to show, given the microscopic amount that the Government Digital Service are paying these "identity providers"?

As soon as the registration process was complete Digidentity started trying to sell the short, fat, ugly, old and smelly one (SFUOS) SSL certificates for his website and digital signature apps for PDFs. Understandably enough, they must need the money.

But that's Digidentity's problem. It's not SFUOS's fault that Digidentity signed up for this commercially nonsensical GOV.UK Verify deal.

And what's SFUOS got out of it?

He can use his new GOV.UK Verify on-line ID to sign into HMRC's website and play with his self-assessment. But he's been able to do that for years, using the Government Gateway. And without telling the Dutch about his mortgages.

What level of assurance do HMRC have as a result of this entirely on-line registration process that the person on the other end of the line really is SFUOS?

Not a high one.

As Digidentity themselves say, if you want adequate assurance, you need face-to-face meetings:

Updated 2.3.15

Last week's Guardian says:

You may be inclined to put this down to the hard left tendencies of the Scottish National Party (SNP).

You may console yourself with the thought that it could never happen in England.

You may be wrong.

Hidden away on the web where anyone can see it is a project called NHS Citizen:

Still, let's take a look at NHS Citizen's ideas about this "simple question".

Their answer is set out in a draft paper, punchily entitled Developing technology infrastructure for NHS Citizen: Discussion paper looking at the technology platforms and standards needed to support the NHS Citizen system design.

Where do citizens live? In countries. And what do countries issue? Currencies. What do we read on p.7 of the NHS Citizen paper, para. 2.3? "Do we need a social currency?" No.

Next question.

Apart from currencies, what else do countries issue to their citizens? Passports. What do we read on p.27 of the NHS Citizen paper, para.5.1? "Why do we need a participation passport?" We don't.

The NHS isn't a country, we aren't citizens of the NHS and the analogy has been pushed too far.

Who's doing the pushing?

There are many hints as you plough your way through to p.27. "Digital by default" turns up three times. As does "agile". And the citizen having "control" over his or her own data appears 19 times, for example here::

Is there anyone left in the world who can't predict the contents of section 5/p.27 et seq. of the report?

Here's one last hint before the inevitable dénouement, p.26, para.4.7.2:

Updated 4.3.15

"Scottish plans for central identity database spark privacy criticism", we said the other day, only to ignite an inferno of anguished enquiries to DMossEsq's Pyongyang-based call centre.

"What Scottish plans for a central identity database?", people wanted to know. "Why aren't the Scots using GOV.UK Verify (RIP) likeevery most a lot of some other right-thinking Brit/Brits?" And "what happened to Government as a Platform – why have we got two identity management systems instead of one?".

Callers are reminded that they are recorded for training and quality control purposes. There's no need for language like that. Nevertheless, these are good questions.

The fact is that the Scots have got their own identity management system, myaccount. Users of Scottish public services can register on-line. 10,000 of them had done so by some time last July, 2014. myaccount has terms and conditions, just like GOV.UK Verify (RIP), only shorter, and it even has a privacy impact assessment, unlike GOV.UK Verify (RIP).

And you never knew, did you. GDS never told you.

GDS said they were the first to come up with a way of creating identities entirely on-line. They're not.

The Scots aren't using GOV.UK Verify (RIP) because (a) they don't want to and (b) they don't have to and (c) because myaccount works with Scottish local authorities and the Scottish NHS and a number of other service providers, whereas GOV.UK Verify (RIP) doesn't. At least, that's what the Scots say.

We haven't got one identity management system in the UK and we haven't got two of them either. We've got hundreds and that's a Good Thing, it constitutes a good solid platform – GOV.UK Verify (RIP) is just one amongst many.

The Scots have got their own GOV.UK as well. It's called gov.scot (or possibly Riaghaltas na h-Alba).

GDS are great advocates of "routing round Whitehall". They can hardly be surprised that other people route round GDS, and neither should you be.

GDS announced their invitation to tender for a new GOV.UK Verify (RIP) framework last year, noted here on 18 December 2014. Were any suppliers recklessly uncommercial enough to bid by the 16 February 2015 deadline? Not long to wait now, you'll find out this month or next, March or April 2015, when contracts, if any, are awarded.

Updated 10.3.15

Here we go again.

How many certified companies are there in the GOV.UK Verify (RIP) framework?

Last week, the following tweet appeared:

So there are three certified companies.

Or are there?

On 15 April 2013, when certified companies were still called "identity providers" and GOV.UK Verify (RIP) was still called "IDA" or "IDAP" – identity assurance or the identity assurance programme – GDS's Steve Wreyford published Delivering Identity Assurance: You must be certified:

Of the three certified companies named in the @GOVUKVerifyRIP tweet above, Experian offer two services which appear on tScheme's list of approved services, Digidentity and the Post Office offer none. So there is one certified company. There aren't three.

Or are there two?

Verizon have a service on tScheme's list of approved services. But according to GOV.UK Verify (RIP) they're not a certified company. Why not?

Perhaps the definition of "certified company" has changed since 15 April 2013. In that case, perhaps GDS would like to tell us what the new definition is.

Make that 11 December 2014. That's when GDS's Janet Hughes published What it means to be a ‘certified company’:

So far we've been restricting ourselves to the five "identity providers" left on GDS's list after Ingeus, Cassidian and PayPal resigned from the first IDA framework. But now there's a second framework heaving into view:

Trust is being demolished through lack of openness. And yet GDS claim to be building trust by being open. It's rum.

Updated 12.9.17

There we were, 1,060 days ago on 18 October 2014, mulling the question of identity:

Experian are an "identity provider" for GOV.UK Verify (RIP). Can you remember GDS's announcement about Experian being fooled into divulging personal information to a conman? No of course you can't, GDS made no announcement at the time and they still haven't.

There's open for you.

And now Equifax have been hacked. "Up to 44m Britons at risk in Equifax cyberattack", as they put it in The Times newspaper. And who are Equifax? A credit rating agency. And you'll never guess, do they have anything to do with GOV.UK Verify? Yes they do. They are sub-contracted to three "identity providers" – Barclays, GB Group and the Royal Mail – and one ex-"identity provider", Verizon.

And have you heard GDS's announcement about Equifax being hacked? No of course you haven't, they haven't made one.

Can Barclays, GB Group and the Royal Mail keep going without Equifax? Can GOV.UK Verify (RIP) keep going based on its a-person-is-a-credit-history model while the credit rating agencies haemorrhage our personal information?

We have no advice on these matters from GDS. They don't seem to care.

Any trust you credited GDS with must surely now be history.

IDA is the Cabinet Office Identity Assurance programme. And it's dead.

----------

The beta test was a private affair. Close family only. GDS (the Government Digital Service), with just HMRC (Her Majesty's Revenue and Customs) and DVLA (the Driver & Vehicle Licensing Agency) in attendance.

Rt Hon Francis Maude MP is the Cabinet Office minister and, as such, the political boss of GDS. Despite all this openness, sunlight and transparency, GDS's trusting public had still not seen IDA for themselves. Ever.

And then on 30 June 2014 we were advised that there is at last a Private beta demonstration available to the public. It was Steve Wreyford again, linking us to OIX and to a video made at the mooncalf conference. A video of GDS's Janet Hughes talking us through IDA:

The video is worth watching. Several times. The presentation comprises 16 slides and there is a set of screen shots available.

The idea is that we shall all need one or more on-line IDs to use public services. Public services should become digital by default. No on-line ID, no services.

The idea is that our on-line IDs should be provided to us by so-called ... "identity providers".

We were led to believe until recently that there are five "identity providers". Judging by this presentation, there are only four left, please see slide #1, Mydex has disappeared.

GDS want to recruit more "identity providers". Thus the mooncalf conference. It's a brave candidate who will put his name forward now, in a field that started with 80 runners and riders/expressions of interest, which then shrank to eight, and from which competent experts like PayPal and Cassidian have subsequently withdrawn.

The application procedure for an on-line ID as demonstrated on 9 June 2014 raises a few hundred questions. Let's make a start with slide #5, which includes this:

By this stage in the application procedure, slide #5, you haven't told GDS who your bank is or who your utility suppliers are. You certainly haven't handed over any logon IDs or passwords to access your accounts.

And yet here's an "identity provider" warning you that they're about to connect to your bank, your utility suppliers, unspecified government departments and unspecified credit referencing agencies to check your details.

Does that mean what it says?

Have the banks and the utility companies and the credit referencing agencies and government departments granted access – access to your personal information – to four companies, the "identity providers", without asking your permission or even, until now, telling you?

"We're building trust by being open"?

----------

Updated 9.9.14

"GDS want to recruit more 'identity providers' ...", we said above, back in July, "it's a brave candidate who will put his name forward now ...". It's September now and this has just arrived, Procurement 2: timeframes and market briefing event, an invitation to a briefing for brave candidates to take place on 30 October 2014.

Book early to avoid disappointment. DMossEsq has. No more than two brave representatives per brave organisation.

NB

The identity assurance team have got their identity wrong.